Building credit might seem a bit complicated if you’ve never done it before. The biggest hurdle to overcome is being able to show a history of responsible repayments to qualify, when you don’t have any credit history in the first place.

To overcome this challenge you need to select what type of building credit option is best for you.

Once you have a full understanding of all of your options, it will be easier to make the right choice for you.

To help you decide we are going to explore these options and make it simple for you to choose one.

We are going to cover the following:

- 4 Ways To Build Credit

- What Is A Secured Credit Card?

- How To Get A Secured Credit Card

- How Do You Use A Secured Credit Card?

- Become an Authorized User

- How Do You Become An Authorized User?

- Get a Credit Builder Loan

- How Does A Credit Builder Loan Work?

- Get a Cosigner

- How Does Getting A Cosigner Work?

- Time To Make a Decision

- Conclusion

So let’s get started:

4 Ways To Build Credit

There are 4 basic ways you can begin building your credit.

- Get a Secured card

- Become an authorized user on someone’s account

- Get a credit builder loan

- Get a co-signer

So what are these different options? How do they work? Can you do this by yourself, or will you need someone’s help?

Getting and using a credit card is the quickest way to build credit. However, it’s hard to qualify for a credit card without any credit history.

This is when secured credit cards come into play.

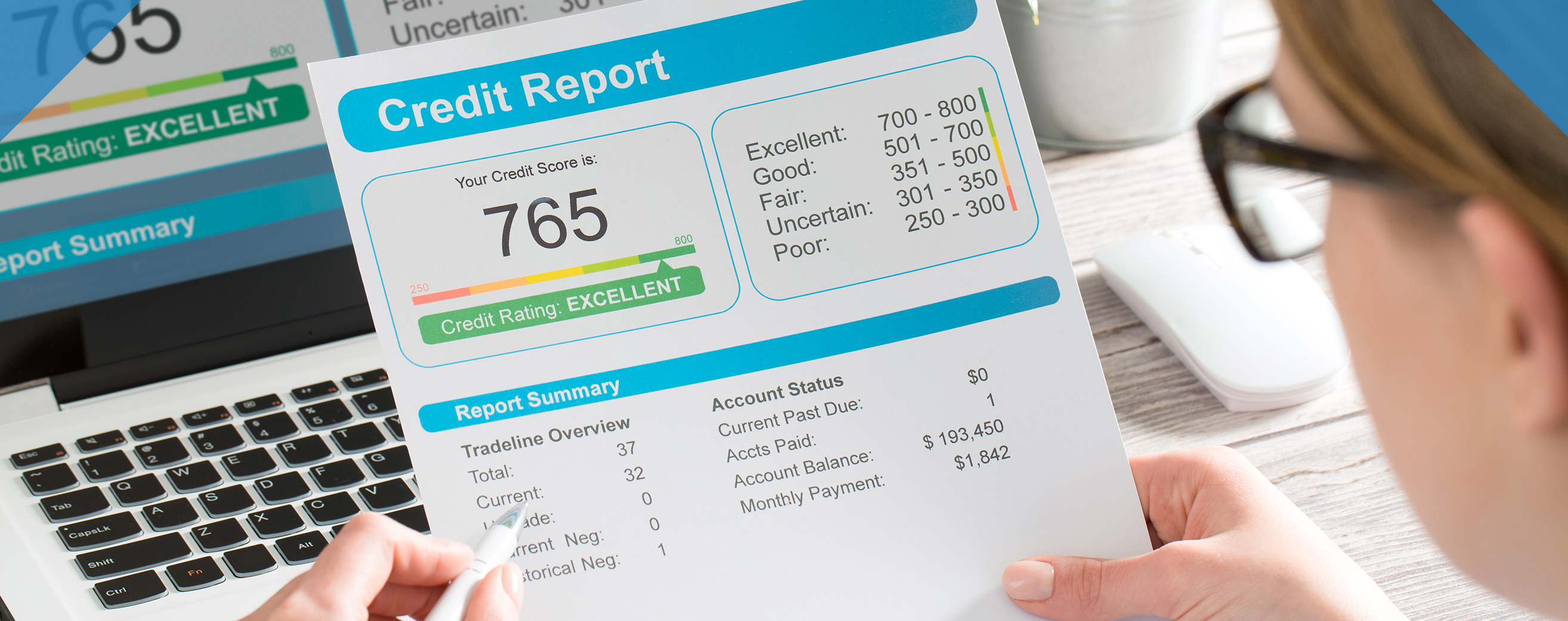

What Is A Secured Credit Card?

A secured card is a credit card that requires a refundable deposit in exchange for a credit limit.

The credit card issuer will retain a security deposit. Typically this deposit is around $200 or more. Once approved, you’ll pay the deposit and that amount will become your available credit limit.

How To Get A Secured Credit Card

Obtaining a secured credit card is pretty simple. You’ll submit an application which should only take a few minutes to complete. Within minutes you’ll know how much of a security deposit will be required.

Once payment has been made, you’ll receive a card with the amount of your security deposit as your credit line.

How Do You Use A Secured Credit Card?

You can use the secured credit card just like any traditional credit card. There are no differences, but we do have some suggestions to help you build good credit right from the start.

- Keep your balance under 30% of your available credit line.

- Exceeding this limit gives off the appearance that you’re overextending yourself and it will cause your credit score to go down.

- So, if you have a $200 credit line, that means you shouldn’t have a balance more than $60.

- Make on time payments

- It’s extremely important to avoid late payments at all times if you want to build a solid credit history.

After all, the security deposit is in place to ensure that the lender recoups their money no matter what.

Example of How To Use A Secured Credit Card

Let’s say you’re looking to start building credit with a secured credit card. You’ll give the financial institution $200 as a security deposit. Then, you’ll be sent a secured credit card with a credit limit of $200.

Remember to keep your credit utilization ratio under 30%, which means you can charge a maximum of $60. Make sure you stay within these limits, and pay the balance off in full at the end of every month. Do not let your balance carry from month to month as you’ll accrue interest and lower your credit score.

As you continue to show responsibility with the card, you may be upgraded to an unsecured card. Once this happens, your security deposit will be returned. By properly handling your unsecured card, you’ll be able to speed up this process and get yourself a secured card quicker.

Improving your ✨CREDIT SCORE✨ isn’t only about correcting past mistakes. One study reports that more than 15 million Americans have no credit at all! 🤯

By taking the right steps from day one to build a solid credit history before you know it! https://t.co/M2peW9slNK#Finance pic.twitter.com/Lmr6NQp1yO

— Get Out of Debt (@getoutofdebtcom) November 19, 2018

Become an Authorized User

Being an authorized user means that you will have a card issued to you, but from someone else’s account. So, you will not be putting in an application on your own.

As an authorized user, you are not legally held responsible for any debt related to that account. The responsibility will fall solely on the primary account holder. However, your credit score will definitely be affected if the card is not paid on time.

How Do You Become An Authorized User?

First, you need to find someone that will trust you with their credit card. This is extremely important, because you’ll have the ability to make purchases on their account.

Once you’ve figured that bit out, it’s as simple as having that person call their credit card company or logging to their online portal to add you as the authorized user.

Isn’t that simple?

Then, you’ll have to wait between 7 to 10 business days to receive a card with your name on it.

Even though this seems very easy, there are some things you need to consider before moving forward with this option. There are some risks that come with being an authorized user.

Some reasons why becoming an authorized user on someone else’s account could hurt your credit score:

- If payments are not made on time

- If more than 30% of their credit line is utilized

- If the creditor does not report the account to the credit bureaus

Any of these things will prevent your score from increasing, and may even cause your credit score to go down.

It’s imperative that you sit down and discuss everything with someone before completing the process. Ask them if they’re willing to share their account balances and payment history with you.

Make sure that whoever you ask to add you to their account is someone you are close with, maybe a family member or close friend. You’ll be asking them sensitive financial information, that not everyone is willing to share.

Get a Credit Builder Loan

When you don’t have any credit, getting a loan is just something that typically just won’t happen. In other words, you are a risk to the lender because they don’t know if you are likely to pay on time or not.

But, a credit builder loan works differently, and this makes it a great place to start building your credit history.

A credit builder loan will show the lender that you’re a responsible borrower who makes on time payments.

How Does A Credit Builder Loan Work?

If you decide that you’d like to take out a credit builder loan, you’ll head over to your local credit union and put in an application. These loans typically range from $300 to $1,000 with an interest rate from 5-16%.

Since these loans are smaller, the monthly payment should be a more manageable amount for you.

Once approved, the money that you intend to borrow will be placed in a savings account which you will not have access to. The money will stay there, like it’s frozen, until it’s paid in full.

You’ll make regular monthly payments during the length of the loan, which will probably be anywhere from 6 to 24 months.

Once the loan is fully paid, you’ll receive the total amount of the credit builder loan.

A good thing about this option is that while you’re making your regular payments on the loan, the loan issuer will be reporting this to the 3 major credit bureaus. This will start showing a history of payments on your credit, which should increase your score.

Something to take in consideration when applying for a credit builder loan is that you will be paying application fees and interest. Double check that you understand all the terms before you agree.

Take your credit score from 😒 to 💪. Check out our list of 7 best credit cards for those with #NoCredit! https://t.co/24TpZ465ad#MondayMotivation #MondayMorning #financialeducation pic.twitter.com/4Nzo6Iej30

— Get Out of Debt (@getoutofdebtcom) October 1, 2018

Get a Cosigner

When you get a cosigner on a loan or line of credit, both parties are responsible for repaying the loan.

That means it’ll show on both of your credit reports. So, if the loan is paid on time, it’ll help build you and your cosigner’s credit. But, if it’s not paid as it should be, both you and your cosigner’s credit will be affected.

How Does Getting A Cosigner Work?

You need to find someone that has good credit and is willing to take on the responsibility with you.

Once you have this in place, both you and your cosigner will complete an application together.

The financial institution that you apply with will take everything into consideration. Once approved, you’ll have a monthly repayment.

Make sure to sort out all of the details with the person going through this process with you. If payments are not made on time, you won’t be reaping any of the benefits of having a cosigner. In fact, you’ll actually be hurting both of your credit scores.

Time To Make a Decision

Before making a decision, ask yourself these questions:

- Do I have money to put towards a security deposit?

- Do I know someone that is willing to add me to their credit card?

- Do I have enough income to take on a loan and pay it without sacrificing my day to day expenses?

- Do I know someone that is willing to cosign with me on a loan and have no issue?

If you can get an affirmative response on one of these, it’s worth looking into that option.

No matter what, you need to make a decision based on your current financial situation and what option will benefit you the most in the future.

Maybe you can’t find someone who is willing to add you as an authorized user or cosign a loan with you. There’s going to be hurdles that you need to overcome. If one option doesn’t work for you, look into the next.

Once you’ve selected an option, see it through and make sure you’re building your credit effectively from the start.

You’ll start to see changes in your credit score around the 6 month mark.

Conclusion

Building credit does not have to be as difficult as it seems. Yes, there are some obstacles to overcome in the beginning. But, we’ve given you four strategies to get going and any one of them will get you where you need to be!

Once you’ve begun the process of building your credit, make sure to stay on top of your score. The last thing you want to do is establish a bad credit history.

What strategy will you use to build your credit? Let us know in the comments!

Leave a Reply