Feeling like all roads are leading towards bankruptcy? Before you take the plunge, it’s important to understand what bankruptcy really is and how it will affect you.

The emotional distress can be overwhelming all on its own. And on top of that, bankruptcy documents come with a lot of legal mumbo jumbo that can be hard to understand.

But don’t worry, we’ve put together a simple guide of the bankruptcy definition explained in a way that anyone can understand.

You’ll learn what bankruptcy is, and how to differentiate between the different chapters. So you will know which chapters you qualify for and how long they will be on your credit report.

With these tools, you’ll be able to make an informed decision for the betterment of your financial future.

We will cover the following:

- What is Bankruptcy?

- Liquidation

- Reorganization

- Bankruptcy Chapters

- Chapter 7

- Chapter 13

- Chapter 11

- Chapter 12

What is Bankruptcy?

Bankruptcy is the process where a person states himself or business is unable to pay the debts owed to their creditors.

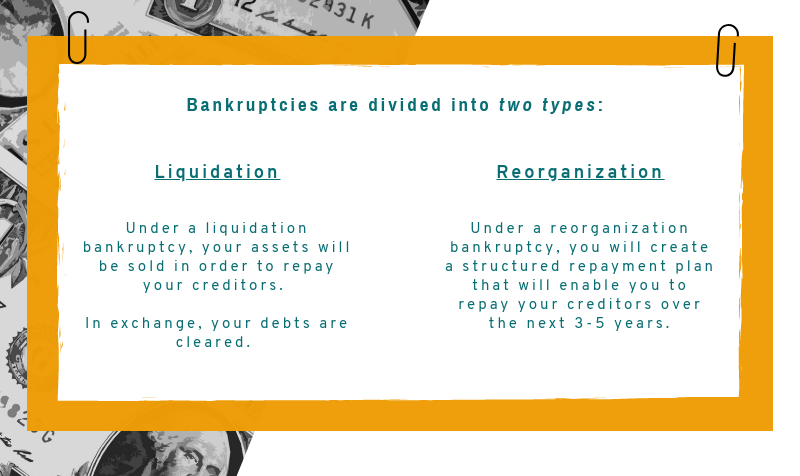

Bankruptcies are divided in two types: liquidation and reorganization.

Liquidation

Under a liquidation bankruptcy, your assets will be sold in order to repay your creditors. In exchange, your debts are cleared. A liquidation bankruptcy is often referred to as a Chapter 7 bankruptcy.

Reorganization

Under a reorganization bankruptcy, you will propose a plan that reorganizes the debts you have. You will create a structured repayment plan that will enable you to repay your creditors over the next 3-5 years. A reorganization bankruptcy is typically referred to as a Chapter 13 bankruptcy.

One or the other may sound more appealing to you, but the truth is you may not get to decide for yourself. It all depends on your specific situation and which chapter you qualify for.

You’ve probably heard of a Chapter 7 or 13 bankruptcy before. That’s because these are the two most common types of bankruptcy. But, they aren’t the only ones.

So let’s take a deeper look into the different chapters to see what each process entails.

Bankruptcy Chapters

Chapter 7

Chapter 7 is an example of a liquidation bankruptcy. Both individuals and businesses are eligible to file this chapter.

As we know, a liquidation bankruptcy involves the selling of your assets in order to clear your debts. When it comes to the liquidation of your property, it will be broken down into 2 categories: non-exempt properties and exempt properties.

Your assets that can be seized and sold as part of paying off your debts are called non- exempt properties.

Non-exempt properties include:

- Second or vacation home

- Second car

- Cash

- Bank account funds

- Stocks and bonds

- Stamp/Coin or other valuable collection

- Family heirlooms

- Musical instruments (unless debtor is a professional musician)

However, some of your assets cannot be taken from you through a bankruptcy filing. These are referred to as exempt properties.

Exempt properties include:

- Motor vehicle (up to a certain value)

- Jewelry (up to a certain value)

- Pensions

- Household appliances

- Furniture

- Clothing

- Tools or equipment needed for your profession

This should give you a better idea of what you’ll be able to keep when you file a Chapter 7 bankruptcy.

Of course, the court doesn’t want you to be destitute. So your car and other necessary assets will remain in your possession.

However, any luxury items like a second home or car will be seized and used to pay your outstanding debts.

The major benefit of filing a Chapter 7 bankruptcy is that all of your unsecured debts will be wiped out. Unsecured debts are those that are not tied to property like your home or car.

This includes:

- Credit card debt (including overdue payments and late fees)

- Collection agency accounts

- Medical bills

- Utility bills (anything that is past due only)

- Business debts

- Money owed under lease agreements

- Revolving charge accounts

This is where you can finally breathe a sigh of relief. Filing a Chapter 7 bankruptcy will ensure that you no longer have to worry about any credit or medical debt that’s been piling up. Any unsecured debt you have will disappear with your bankruptcy and you never have to think about it again.

Should you declare #bankruptcy? Consider these questions before you go down the rabbit hole.#finances #money #business #tips #getoutofdebt #moneymatters pic.twitter.com/shWqFOI2vr

— Get Out of Debt (@getoutofdebtcom) May 8, 2018

But, when it comes to your secured debts, it gets a little more complicated. In a Chapter 7 bankruptcy the debtor has to decide between:

Allowing the creditor to repossess the property that is securing the debt, and continue making payments on that debt

or

Paying the creditor a sum of money that will replace the value of that property that is securing that debt

Which route you end up taking will depend on your financial circumstances. Obviously, filing bankruptcy means that you’ve hit a bump in the road when it comes to managing your money. So, paying your creditor an amount equal to your property may not be a plausible option for you right now.

However, if you are able to pay your creditor for the secured asset, you will be able to keep it. If you are not able to pay your creditor, they will repossess the property, and you will continue to make regular payments on it.

You should expect the entire process of filing a Chapter 7 bankruptcy to take between 3 and 6 months from start to finish. Once the bankruptcy has been discharged, it will remain on your credit report for 10 years.

Chapter 13

Chapter 13 is an example of a reorganization bankruptcy for individuals. It’s also known as the “Wage Earner’s Plan” because you need a reliable source of income in order to file this chapter.

This is because your unsecured debts will NOT be wiped out like they are with a Chapter 7 filing. Instead, you will work with the federal court to create a repayment plan that you will follow for the next 3-5 years, until your creditors are paid.

There’s 3 things you need to pay attention to when it comes to a Chapter 13 bankruptcy:

- Paying off debt

- Limits on debt

- Repaying secured debts

Paying Off Debt

A Chapter 13 bankruptcy involves paying back your unsecured debts. You’ll do this through a repayment plan that the federal court approves.

So you’re probably asking yourself, “How much will I need to pay?”

Well, it’s based off of a couple of different factors. The first two are your income and the amount of debt you owe. Next, the court will look at how much your creditors would have received on your unsecured loans if you had chosen to file a Chapter 7 instead.

Limits On Debt

There’s also a limit on the amount of debt you can put under your bankruptcy. The limits associated with filing a Chapter 13 bankruptcy are subject to change every three years.

As of April 1, 2016, the limit on secured debt is $1,184,200 and the limit on unsecured debt is $394,725.

If you exceed these limits, you may not be eligible to file for a Chapter 13 bankruptcy.

Sometimes, we #spend beyond what is necessary. So here are helpful #creditcard tips to lead you out of #debt! https://t.co/HUyKCNnUON #debtfree #financialfreedom #creditscore #moneymatters pic.twitter.com/GUz2EJzLMp

— Get Out of Debt (@getoutofdebtcom) April 29, 2018

Repaying secured debts

Like in a Chapter 7, you may be able to repay some of your secured debts when filing a Chapter 13, even if you are behind on the payments.

In a Chapter 13 bankruptcy the debtor has to decide between:

The property being sold and wrapping the remaining amount owed to the creditor into the court appointed repayment program

or

Paying the creditor for the property in full, usually with interest, through the court appointed repayment plan

Once your Chapter 13 bankruptcy has been discharged, it will remain on you credit report for 7 years.

Like we said earlier, Chapter 7 and Chapter 13 are the two most common types of bankruptcy filed. Chapter 7 is an example of a liquidation bankruptcy, while Chapter 13 is a reorganization of your debt.

But, there are additional chapters that you need to know about. These are Chapter 11 and Chapter 12. They are both examples of a reorganization bankruptcy.

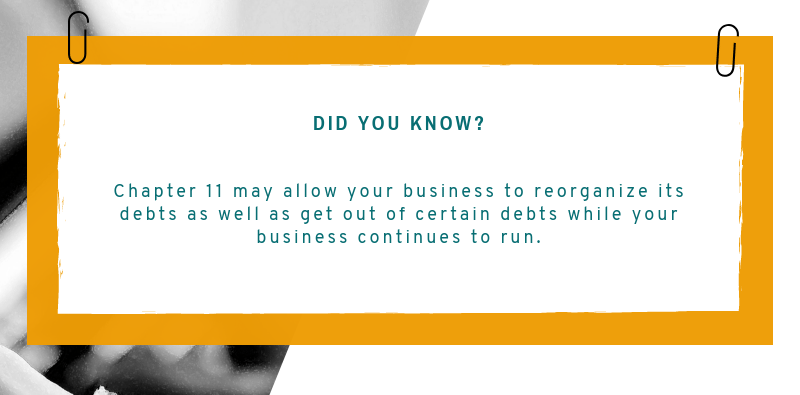

Chapter 11

Businesses and individuals may both be eligible for relief through a Chapter 11 reorganization bankruptcy, although it most commonly used by corporations.

You may be surprised to find out that filing a Chapter 11 bankruptcy does not mean the business will close its doors. In most cases, the business will remain open and continue to be run as usual. However, you may be banned from making certain decisions regarding business operations without the permission of the court.

The goal of filing a Chapter 11 bankruptcy is to become profitable as opposed to closing the doors. When you file, you’ll be able to propose a plan for how the business will be profitable post bankruptcy.

This could include:

- Cutting costs

- Finding new sources of revenue

- Downsizing operations

- Renegotiating debts

- Liquidating assets

Once the plan has been approved by the court, creditors will be paid in accordance to it.

While Chapter 11 was initially intended for businesses, some individuals may be eligible as well.

However, a Chapter 11 bankruptcy will typically be a much more expensive process than the other filings. So why would an individual file a Chapter 11 over a 7 or 13?

Remember those debt limits on a Chapter 13?

Those don’t exist with a Chapter 11. So if you’re over those limits, you’ll be disqualified from filing a Chapter 13 and be forced into a Chapter 11.

If you own a large amount of non-exempt properties and do not want to liquidate them as you would in Chapter 7, this may be a good alternative for you.

It will take a few months, up to 2 years, for a Chapter 11 bankruptcy case to be complete. Once it is discharged, it will remain on your credit report for 10 years.

Chapter 12

A Chapter 12 bankruptcy is extremely similar to a Chapter 13, with one exception. The only difference between them is that family farmers or family fisherman are the only ones eligible to file a Chapter 12.

More specifically, 80% of the debt involved in the case must come from a family farm, and the debtor must have sufficient income.

Just like with a Chapter 13, the debtor will propose a repayment plan to pay their creditors over the next 3-5 years. The court must finalize this agreement.

Once the bankruptcy has been discharged, it will remain on your credit report for 7 years.

So, there you have it. The 4 different types of bankruptcies laid out in a way that anyone can understand. By now you should have a better idea of what bankruptcy chapter will benefit you the most, and what you can expect when you file.

Are you considering filing bankruptcy? Would you prefer a liquidation or reorganization? Let us know in the comments!

Leave a Reply