A lot of people believe that renters insurance is going to affect their monthly cash flow the same as having another credit card or loan payment.

The reality is that it’s NOT! People are not protecting their things like they should just because they are just not well informed.

In this article we are going to answer some common questions and go over the important aspects of renters insurance. All of this will help to make sure that you have all the information you need to go out and get yourself protected!

Throughout this article we are going to cover the following:

- What Is Renters Insurance?

- What Factors Impact The Cost of Renters Insurance?

- Variable Factors When Choosing Renters Insurance

- How Much Renters Insurance Do You Need?

- How Much Is Renters Insurance?

- The 5 Cheapest States for Renters Insurance

- The 6 Most Expensive States for Renters Insurance

- Do You Need Renters Insurance?

- Conclusion

So let’s get started and explore the benefits of having a renters insurance.

What Is Renters Insurance?

Renters insurance is put in place to protect renters like you from any financial loss if there were to be any damage to your property due to an unexpected event.

The reality is that unexpected events happen all the time. Everyday we hear about things like fires, vandalism, floods, theft and natural disasters. These things are taking place in our communities, and all over the world.

With renters insurance in place, you won’t have to worry about the after effects of any of these, because you’ll be completely covered.

When it comes to figuring out how much you will pay under a renters insurance, it can be a bit tricky. There are certain factors that will impact the cost of your premium. So, don’t expect to get the exact quote that your neighbor did.

What Factors Impact The Cost of Renters Insurance?

Certain factors will impact the cost of your insurance, like:

- Your location: Renters insurance rates will vary by state, cities, and neighborhoods. It’ll take into account areas that are prone to devastating natural disasters, high crime rates and even the age of the property. For instance, an older building is going to cost more to insure than a newer structure.

- Your credit score: Your credit score will be an important determining factor when establishing your renters insurance rate. Your score will be looked at to determine whether or not you’re a high risk borrower. The higher your credit score is, the lower your premium will be.

- Value of your belongings: Your rate will also be determined by what you own, and the value of those items. The higher the value, the more your insurance is going to cost you. Simply put, you’re going to need to pay more upfront in order to protect any assets that are extremely valuable.

These factors are pretty much already determined. Your location under this policy isn’t going to change, and chances are the value of your belongings and your credit score won’t move much either. But, there are certain factors that determine your renters insurance that you do have complete control over.

Variable Factors When Choosing Renters Insurance

The following factors are variable, and will affect your rate based on the decisions you make. And hey! Everyone will select what they believe is best for them. So here are your options:

- Amount of Coverage: The more coverage you have, the more it’s going to cost you. It’s really going to come down to whether you want to pay a lower or higher premium.

- If you are willing to accept a lower payout if an unexpected event were to happen, then you can opt for a lower premium.

- If you want a higher payout if an unexpected event were to occur, then you should opt for the higher premium.

- Deductible Amount: This refers to the amount of money you’ll be required to pay out of pocket before your coverage kicks in and begins to pay you.

- The higher your deductible, the lower your premium will be.

- The lower the deductible, the higher your premium will be.

- Reimbursement Post Claim: When you place a claim, there are 2 ways for the insurance company to reimburse you.

- Actual Cash Value Renters Insurance: If you go this route, you’ll be reimbursed the cost of replacing your belongings, minus depreciation from the time you placed the claim. This means that you will not be reimbursed the price that you paid upon purchasing. This option makes for a lower premium.

- Replacement Cost Renters Insurance: If you go this route, you’ll be reimbursed the cost of replacing your items with brand new ones. This means your provider will pay more in the event of a claim, which will drive your premium up.

How Much Renters Insurance Do You Need?

The amount of coverage you need will be determined by your personal circumstances. It’s going to depend on the value of your personal belongings, as well as the liability coverage you choose.

So, how do you determine these numbers?

- Take Inventory of Your Belongings

The first thing you need to do is take a home inventory of your personal things. By doing this, you’ll have a better idea of the level of coverage you’ll need and how that will affect the cost of your renters insurance policy.

Determine the value of your belongings, and be sure not to underestimate them!

The best way to get the closest number to the actual value is by:

- Walk through each room of your rental property

- Describe each item and include the quantity

- Write the serial number for each item and their purchase date. (If you don’t have the actual receipt, you can estimate the purchase date).

- Take pictures of your belongings

- Store this information in a safe place other than your home. Make sure you can access the information from other locations in case of an unexpected event at home.

- Consider Liability Coverage

If you have a liability coverage and someone gets injured on your rental property, it may help cover legal fees, as well as medical costs.

Legal expenses can become very expensive. So, analyze in detail how much liability coverage you need, and make sure you add the proper amount to your policy.

Once you have done this, your insurance company will be able to determine coverage limits on your items.

Make sure to take note of your most expensive items! Things like:

- Electronics

- Jewelry

- Valuable collectibles

You’ll want to determine if you need any additional insurance to keep these valuable belongings protected. Don’t forget that any coverage add ons to your policy will contribute to a higher premium.

After going over all of this information and making sure you know how much coverage you need, it’s time to request a quote from a renters insurance company.

Make sure to be ready before calling!

T give you an idea of how much people are paying now a days, we have gathered some information from the National Association of Insurance Commissioners (NAIC) to provide the following information.

How Much Is Renters Insurance?

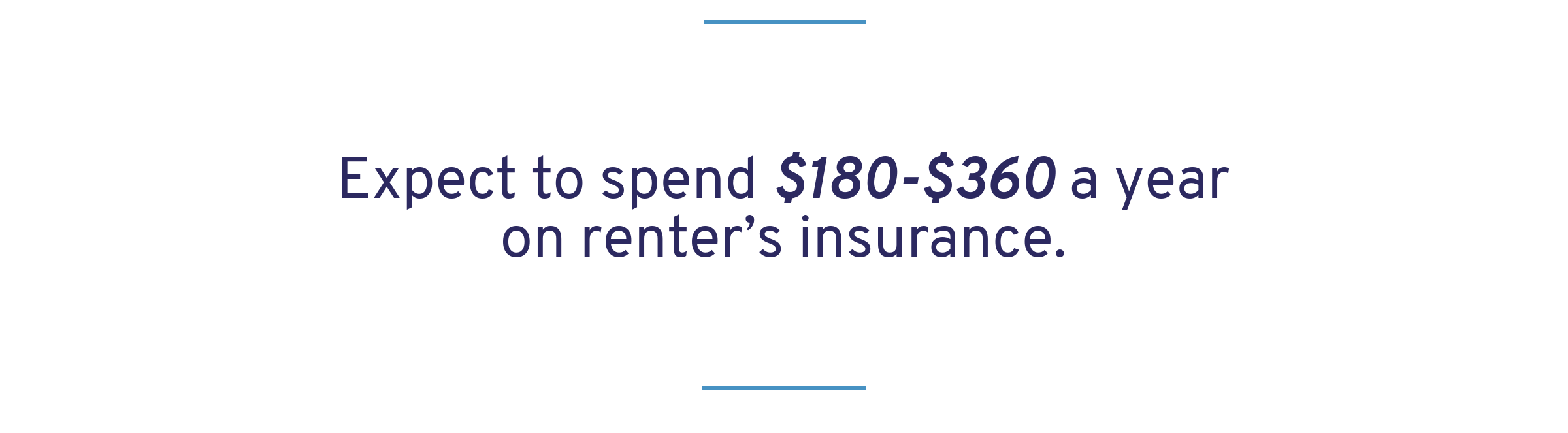

On average, renters insurance costs between $15 to $30 per month, depending on the location, size of the rental property, and the policyholder’s belongings.

But this is nothing compared to all of the benefits that you get by having one.

Some states will have a higher premium because they are more exposed to hurricanes, tornadoes and even severe thunderstorm damage.

Want to save money while living on a tight #budget? It’s possible! Here’s how: https://t.co/P2jwXdkDxo #debtfree #financialfreedom #moneymatters #debt #tips #GOOD pic.twitter.com/gY5eouB9rM

— Get Out of Debt (@getoutofdebtcom) April 17, 2018

The 5 Cheapest States for Renters Insurance

Usually, the states that are far away from natural disasters and extreme weather will come with cheaper renters insurance rates.

If you’re thinking of moving soon and want to calculate what your expenses in your new place might be, it’ll be important to include an estimation of your renters insurance.

The top 5 cheapest states for renters insurance on a yearly basis are:

- North Dakota: $114

- South Dakota: $121

- Wisconsin: $132

- Minnesota: $144

- Iowa: $146

The 6 Most Expensive States for Renters Insurance

The most expensive states for renters insurance are the ones where severe weather conditions like strong storms or tornadoes are more common.

The top 6 most expensive states for renters insurance on a yearly basis are:

- Mississippi: $262 (due to severe storms)

- Louisiana: $249

- Alabama: $242

- Texas: $241

- Georgia: $226

- Oklahoma: $242 (due to tornadoes)

Do You Need Renters Insurance?

Having renters insurance is a smart idea, but you’re not obligated to have it.

If you do opt for a renters insurance policy, you’ll avoid paying out of pocket for any stolen or damaged property.

Plus, if you opt for liability protection, you won’t have to worry about additional medical or legal fees if someone was to get injured in your home.

So, renters insurance seems like it’s a great idea for you. How do you get started?

Steps to Get Renters Insurance

- Determine what your landlord’s insurance policy covers

- Do your research and learn about the different options when it comes to rental insurance policies.

- Compare insurance companies and rates. If you already have auto insurance, look into seeing if you can bundle your policies and save.

- Determine the value of your belongings and the amount of coverage you’ll need for them.

- Inquire with multiple insurance companies for quotes. Explore your options and don’t go with the first one you talk to!

Conclusion

Renters insurance is an inexpensive option that will protect you and your belongings in case of an unforeseen event. By having renters insurance, you won’t have to worry about paying out of pocket for unexpected damages.

While it’s not mandatory, it does come with some great perks.

Do you have renters insurance? Let us know in the comments!

Up Next: 7 Best Renters Insurance Options

Leave a Reply