Are you at the point where you can’t afford more than your minimum payments every month? Are your credit card balances just continuing to increase with every statement?

If so, you’re probably ready to throw your hands up and scream.

Odds are that you’ve exhausted all of your options at this point. You don’t know where to find any additional money to put towards your debts.

So what do you do now?

You might have heard of debt settlement before. Where people settle their debts for less than they actually owe. Sounds like the perfect solution for your problem, right?

So let’s take a look at some important information on how debt settlement works. Then, we’ll explore the pros and cons. So you can decide if debt settlement is the right path for you to take.

In this article, we’ll cover:

- How Does Debt Settlement Work?

- Hire A Debt Settlement Company

- Negotiate Your Debt Settlement On Your Own

- Hire A State Licensed Debt Settlement Attorney

- Respond To A Debt Settlement Letter Sent By Your Creditor

- Rebuild Your Credit Post Debt Settlement

- The Pros and Cons of Debt Settlement

How Does Debt Settlement Work?

Depending on how the debt settlement process is initiated, there’s a couple of different scenarios that you could expect.

There are 4 ways for a debt settlement to be started:

- Hire a debt settlement company

- Negotiate your debt settlement on your own

- Hire a state-licensed debt settlement attorney

- Respond to a debt settlement letter sent by your creditor

So let’s break down what each of these processes will mean for you and your specific circumstances.

Hire A Debt Settlement Company

A debt settlement company will use their experience to negotiate the best possible settlement offer possible on your behalf. They will talk to you about your situation, and together you’ll determine a plan to start tackling your debts one by one.

So what should you expect if you go with a debt settlement company?

Here’s an overview of the process.

The Debt Settlement Process

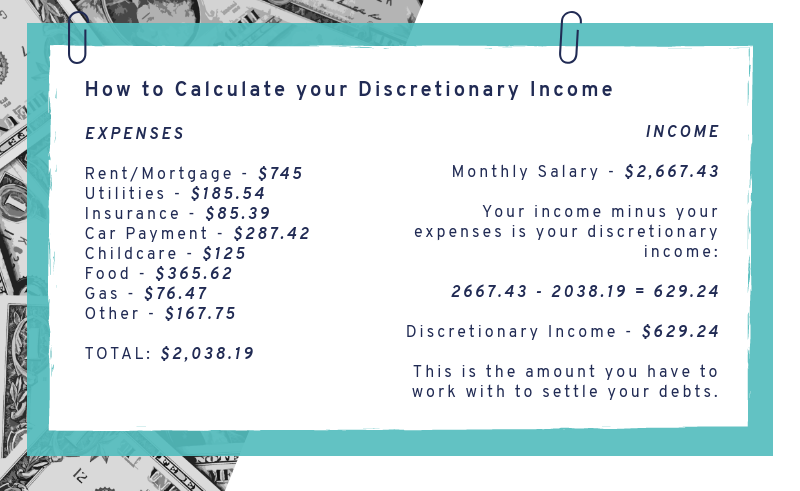

The first thing thing you need to do is determine how much money you’ll be able to set aside to put towards your debts.

In order to do this, you’ll need to create a budget. Start by subtracting your monthly expenses from your monthly take home pay. The remaining amount is your discretionary income.

Here’s an example to get you started:

From that, determine how much of your discretionary income you’ll be able to dedicate to paying towards your debts every month.

Once you’ve done this, you’ll open a new bank account. This is where you’ll put any money you’re going to use for your negotiations.

At this point, the debt settlement company will advise you to stop paying your creditors.

After you’ve saved a sufficient amount of funds in your bank account, the debt settlement company will begin negotiations with your creditors or collection agencies.

Negotiations can take some back and forth before a settlement is reached. Once a settlement is agreed upon, you will most likely make a lump-sum payment to your creditor.

Once the payment is received, your creditor will discharge the remaining debt and the account is closed.

The settlement will be reported to the credit bureaus and will remain on your credit report for 7 years.

Negotiate Your Debt Settlement On Your Own

Did you read the above and think, “Why hire a company? It sounds like I can do this on my own.” Well, you’re right. You can absolutely take on your creditors by yourself.

All you have to do is call each creditor and negotiate your own settlement. So what should you do to ensure you have the best shot at getting a good settlement offer?

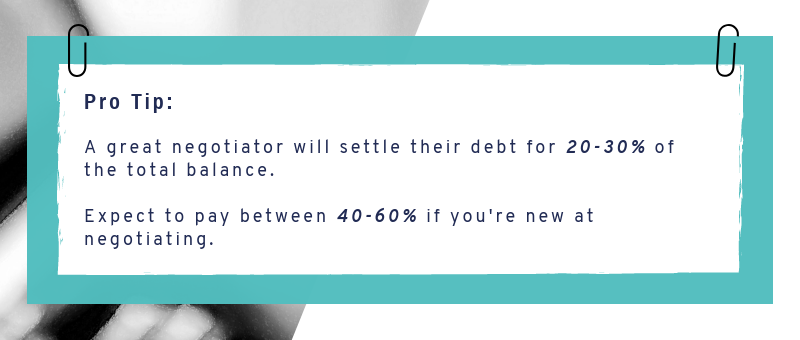

Make sure your offer is reasonable. While you should make your initial offer below your budget, you need to make sure it’s realistic. Most creditors won’t accept a settlement of 5-10% of your balance.

The average settlement is around 48%. The more you do it, the better you’ll get at it. So don’t be surprised if you can’t get your creditor down as much as you thought you could on your first try. That’s one of the reasons why most people like to leave it to the professionals.

Remember that you’ll have a better shot of getting a good settlement offer if you’re able to make it in a lump sum payment. Creditors like this because it’s a done deal.

Agreeing to a repayment plan doesn’t guarantee them that they’ll see their money. So, if you can offer a lump sum, you’ve got a much greater chance of closing the deal.

As the debt gets older, the creditor is expecting to get it back less and less. Use this to your advantage. Your older debts are going to be the easiest ones to negotiate.

Hire A State Licensed Debt Settlement Attorney

A state licensed debt settlement attorney can take you through the debt settlement process as well. This is a great option if you’re being sued by a collection agency because they’ll be able to handle your negotiations as well as your legal issues.

First things first, meet with your perspective attorney and confirm that they are state licensed. Some scammy debt settlement companies may try to pose as a law firm. They will not allow you to schedule an in person meeting with your attorney. If this happens, take it as a red flag and move onto the next.

Once you have selected an attorney, give them an overview of your situation. Fill them in on all of your debts, and any communication you have had with your creditors or collection agencies. Make sure they’re aware of what kind of budget you’re working with, and work together to set realistic expectations for the process.

Your attorney will handle the negotiation process for you, and also advise you if there’s any other legal actions you should be taking.

Understand what #bankruptcy is to know if it’s the best solution for you and your #business. Learn more here: https://t.co/JnPMjvWd9s#tips #money #finance #debt #GOOD pic.twitter.com/onC9QP4JaK

— Get Out of Debt (@getoutofdebtcom) April 2, 2018

Respond To A Debt Settlement Letter Sent By Your Creditor

Most creditors aren’t going to wait around for you to reach out to them. They want their money, and they’re going to be aggressive about getting it.

They will constantly be calling you and sending you mail. This mail might contain debt settlement offers. This is another option you have to settle your debts.

If this is the route you want to take, your first step will be to verify that the debt is yours and that it’s not past the statute of limitations.

If the debt is past the statute of limitations, you’re off the hook and cannot be sued. Simply send them a cease and desist letter that you do not want to be contacted anymore.

If the debt does belong to you and is collectible, review the offer in the letter and decide whether it will work for you or not. You can accept the initial offer, or you can make a counteroffer.

If you’ve never written a debt settlement letter before don’t worry, we have an article which details out the steps for you. Check it out: How To Write A Debt Settlement Letter.

If you’re not comfortable making a counteroffer on your own, you can always seek the help of a professional debt settlement company. Make sure you tell them about the letters you have received and what you can really afford.

Rebuild Your Credit Post Debt Settlement

It’s important to understand that debt settlement will have a negative impact on your credit score. The settlement will remain on your credit report for 7 years from the date the account went delinquent.

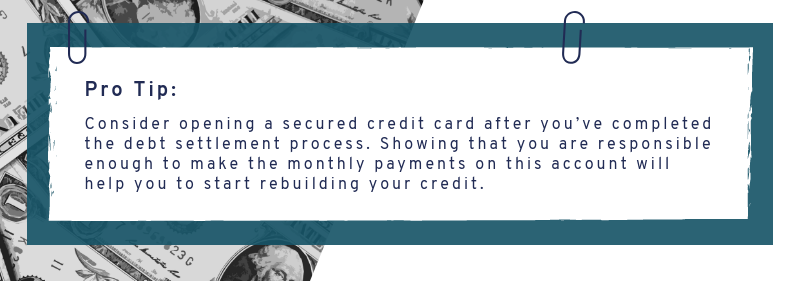

However, negative items account for less and less as time goes by. So by making good choices that’ll improve your score now, you’ll be able to diminish the negative effects of your past debt settlement.

You have the ability to start rebuilding your credit right away and you should take advantage of this. So what kind of things are important to pay attention to?

Keep an eye on:

- Keep your debts to a minimum

- Make payments on time

- Don’t open any new accounts within a 6 month period

- Keep your credit utilization ratio under 30%

- Keep old accounts in good standing open

Remember all those bad choices that got you into this situation in the first place? Play it smart, and let those old habits go. Going forward you need to make smart choices that will allow you more financial freedom in the future.

The Pros and Cons of Debt Settlement

Debt settlement is the fastest and most cost-effective way to get yourself out of debt without declaring bankruptcy.

One of the great things about debt settlement is the fact that you’re in control over how long the program will take you. Depending on your situation, you could be debt free in as little as 12 months. However, the program typically takes from 3-5 years to complete. This will all depend on how much you’re able to save in your seperate savings account.

No matter if it takes you 1 or 5 years to complete the program, it’ll be nothing compared to the years of stress you’ll experience trying to pay your cards off on your own. Not to mention the fact that you’ll finally get your creditors off of your back while avoiding bankruptcy.

The icing on the cake? You’ll only have to pay a fraction of what you actually owe.

But, every action has its consequences too.

Debt settlement forces you to become delinquent on your open accounts. When this happens, your balance will initially increase. This is due to accumulating interest and late fees. Defaulting on your accounts will also cause your credit score to drop.

These negative marks will remain on your credit report for 7 years.

While you are going through the debt settlement process, you can still be sued by your creditors or collection agency. It’s not a common occurrence, but don’t be caught off guard if it does happen.

Some creditors are notoriously harder to deal with when it comes to negotiating your debt down. Your creditor is not required to accept a debt settlement offer. However, their job is to collect as much as they can so they don’t have to charge off the account. So, your chances of striking a deal are much more likely.

Pros

- Fastest way to get out of debt

- Drastically reduce your debt

- Flexible payment arrangements

- Can be completed in 1-5 years

- Great alternative to bankruptcy

Cons

- Your credit score will be negatively affected

- Creditors are not required to accept your settlement offer

- Debt balances will increase before negotiations start

- Collection agencies will begin to harass you

- Usually takes at least 6 months to make the first settlement

- Your discharged debt is taxable

Conclusion

We know that being in debt can be very stressful. Even making a decision on the best plan of action to get yourself out of debt can be just as frustrating.

We hope you’ll take into account all of the information we’ve provided on how debt settlement works when deciding what’s right for you.

Do you think the pros outweigh the cons when it comes to debt settlement? Let us know in the comments!

Leave a Reply